Samsung Tentpole

Samsung Electronics (005930.KS) reported full 3Q results that were basically in line with guidance. It was no surprise that Samsung’s memory business saw improvement as memory prices continued to increase throughout the quarter, so our focus here is on Samsung’s other businesses. Before we go further it is important to understand how Samsung’s business segments are broken out.

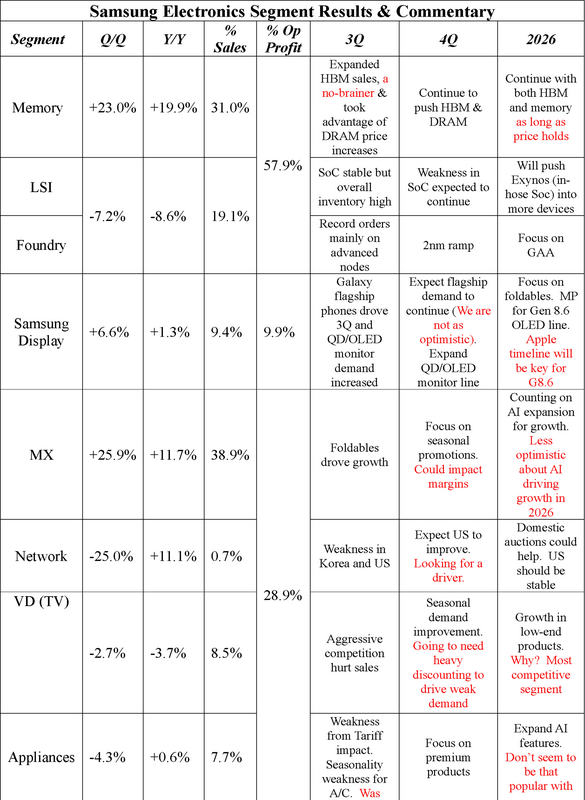

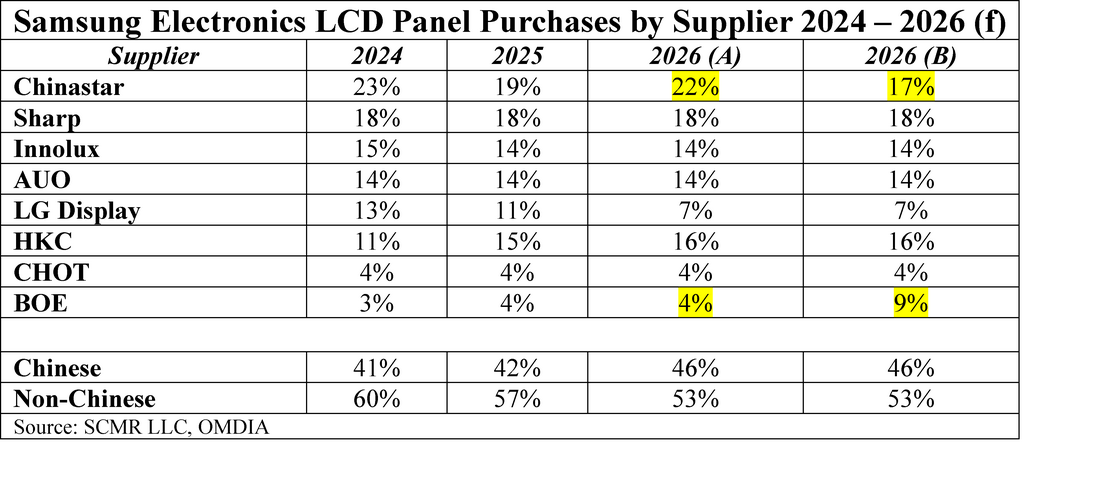

Here we summarize 3Q results, guidance, and 2026 forecasts. Our comments are in red

- DX Division (Device Experience) – Consumer Products

- MX Division (Mobile Experience) – Phones, tablets, laptops, wearable

- Networks – Telecom equipment (4G, 5G, RAN, Infrastructure

- Visual Display – TVs, Monitors, Signage, Projectors

- Digital Appliances – Kitchen & Laundry Appliances

- DS Division (Device Solutions) – Semiconductors, Components

- Memory – DRAM, NAND, HBM, SSD

- System LSI – SoC, Display Drivers, Power Management

- Foundry – Fabrication

- Samsung Display – Display manufacturing

- Harman – Automotive Displays

Here we summarize 3Q results, guidance, and 2026 forecasts. Our comments are in red

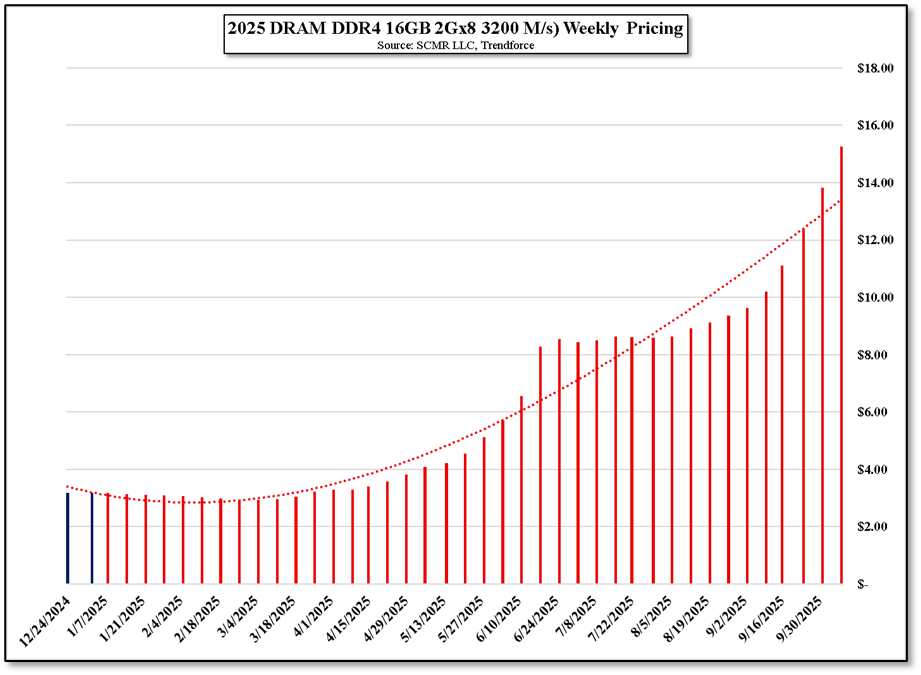

As can be seen from our comments, some of the Samsung commentaryrhetoric does not make sense and seems to be corporate ‘speak’ rather than a hint at real product direction. In other areas (AI appliances, Ai smartphones) we disagree with how much AI will drive incremental sales and see anticipatory buying and Chinese subsidies ending as headwinds in 4Q. That said, Samsung’s memory business, the company’s pariah only a few quarters ago, saved the day and it looks like that will continue into 4Q and early 2026. Unfortunately there is little positive to say about Samsung’s TV business, although TV issues are more industry oriented than particular to Samsung, although the TV line could use some pruning in terms of the number of TV set offerings. All in it was a good quarter because of memory and that looks to continue into 4Q. As long as Samsung’s consumer oriented businesses don’t fall off a cliff the memory business will be the tentpole again in 4Q.

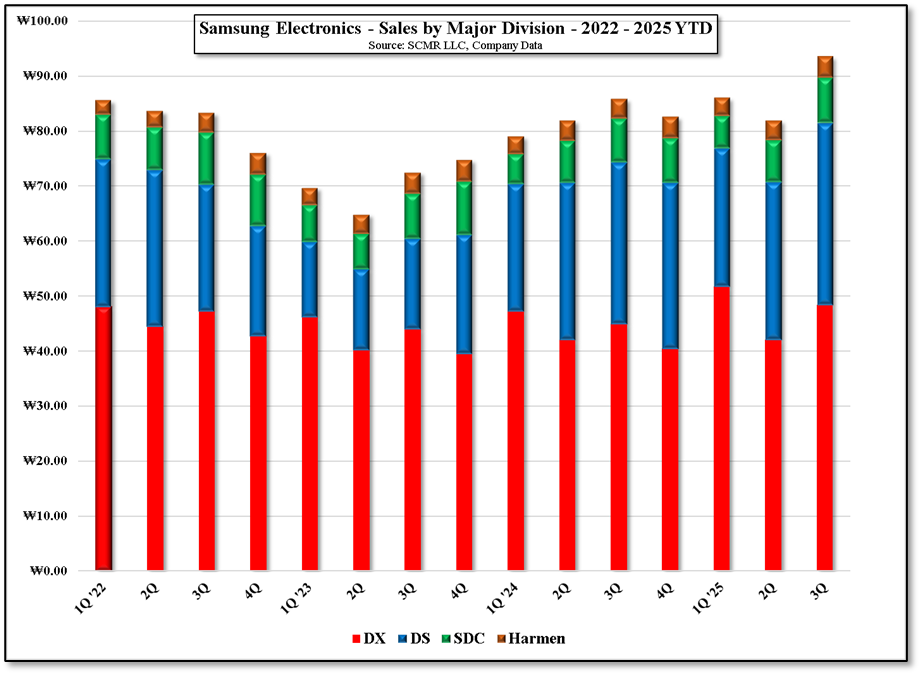

Figure 1 -0 Samsung Electronics - Sales by Major Division - 2022 - 2025 YTD - Source: SCMR-LLC, Company Data

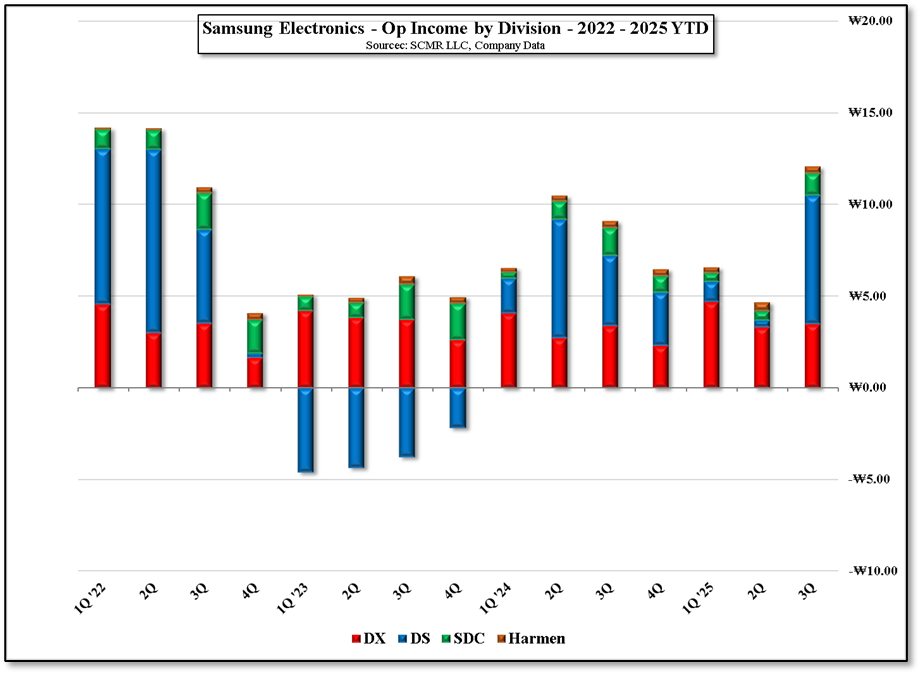

Figure 2 - Samsung Electronics - Op Income by Division - 2022 - 2025 YTD - Source: SCMR-LLC, Company Data

RSS Feed

RSS Feed